Ghana's energy sector is attracting serious capital hedge funds, wealth managers, and private equity are moving into natural gas infrastructure and renewables as the country's IMF-backed stabilisation program begins to recalibrate risk perceptions and reopen the investment pipeline.

Local bank executives report increased interest from institutional and private capital targeting both natural gas infrastructure and renewable energy projects, as Ghana navigates its post-restructuring recovery phase. According to the African Development Bank (AfDB), Ghana's energy transition strategy combines gas-fired generation with renewable energy expansion a hybrid model designed to stabilise electricity supply while reducing long-term carbon intensity.

The renewed investor interest follows Ghana's fiscal consolidation under its IMF-supported program, which aims to restore macroeconomic stability, improve debt sustainability, and rebuild investor confidence. These reforms have begun to materially recalibrate risk perceptions particularly in infrastructure-linked sectors where long-term returns are tied to stable policy environments.

Sources: AfDB, World Bank • Calculations & Modelling: Limitless Beliefs Consulting

Gas as the Bridge — Renewables as the Destination

The investment allocation reflects Ghana's strategic reliance on natural gas as a transitional energy source while renewable capacity continues to expand. Gas infrastructure provides the baseload stability that is critical for industrial activity and grid reliability a non-negotiable requirement for an economy in recovery mode that cannot afford power supply uncertainty.

From a financing perspective, energy projects in Ghana are increasingly structured to attract blended capital. Local banks, international lenders, and private investors are participating in syndicated financing arrangements, often supported by multilateral guarantees. This structure reduces individual risk exposure and enables project development at a scale that no single institution could finance alone.

Ghanaian banks are expanding their project finance capabilities, leveraging improved liquidity conditions and stronger balance sheets following the macroeconomic adjustment cycle. Regional banking data from the AfDB and World Bank confirms that infrastructure lending is becoming a more prominent segment within African banking portfolios and energy is the dominant allocation.

“Energy projects are functioning as a bridge between macroeconomic recovery and long-term structural growth — and institutional capital is finally crossing it.”

Sources: AfDB, IMF, World Bank • Calculations & Modelling: Limitless Beliefs Consulting

Why Hedge Funds Are Looking at Ghanaian Energy Assets

The prominence of energy within infrastructure lending reflects its foundational role in economic systems. Reliable power supply underpins industrial production, services, and digital infrastructure — making energy investments a priority for both public and private capital regardless of the broader macroeconomic cycle.

Hedge funds and wealth managers are increasingly targeting these assets due to their long-term revenue visibility. Energy projects typically operate under power purchase agreements (PPAs) that provide predictable cash flows over 20 to 25-year horizons a structure that aligns with the investment mandates of institutional capital seeking stable, inflation-resistant returns in a high-volatility global environment.

However, currency risk remains a central structural consideration. The Ghanaian cedi has experienced significant periods of volatility, affecting the cost structure of projects and the repatriation of returns for dollar-denominated investors. The IMF has emphasised the importance of exchange rate stability and fiscal discipline in maintaining the investor confidence that Ghana has worked hard to rebuild.

To mitigate these risks, financing structures frequently incorporate dollar-denominated contracts or hedging mechanisms. Multilateral institutions play a complementary role by providing guarantees that reduce exposure to currency and political risks effectively extending their credit quality to projects that would otherwise carry sovereign risk premiums.

Sources: AfDB, World Bank • Calculations & Modelling: Limitless Beliefs Consulting

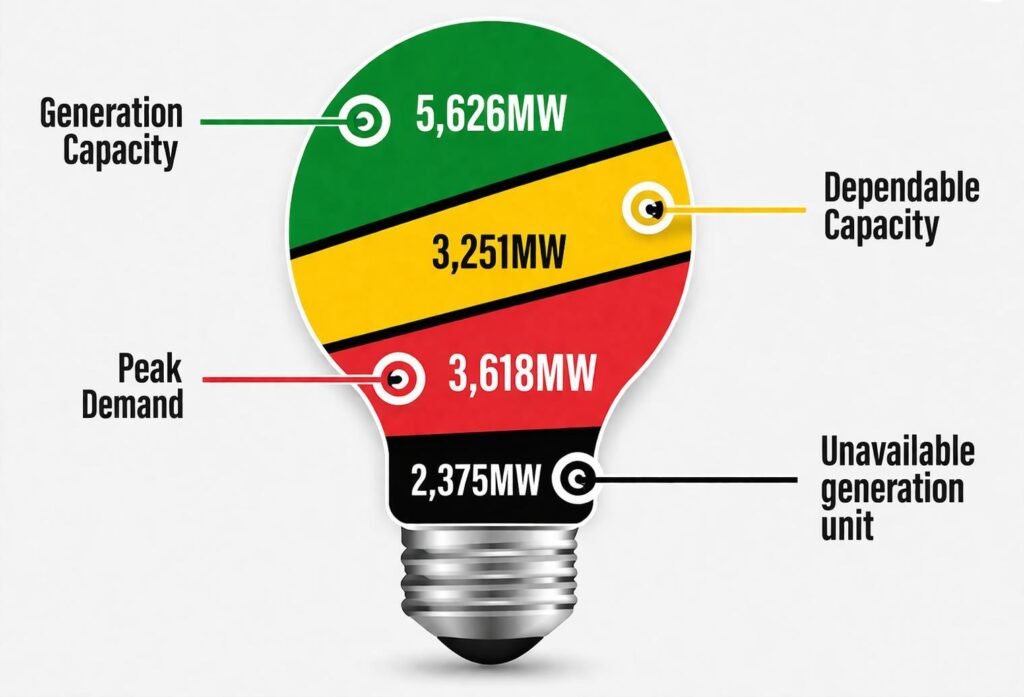

Demand Is Not Waiting for the Policy Cycle

The rising demand trajectory underscores the scale of investment required to maintain grid stability and support economic growth. As urbanisation accelerates and industrial activity recovers, the need for both generation capacity and transmission infrastructure becomes more pronounced demand is not a policy variable, it is a demographic one.

The World Bank has identified energy access and reliability as critical constraints on economic performance across sub-Saharan Africa. For Ghana specifically, the AfDB projects a gradual growth rebound as fiscal consolidation measures take effect and energy infrastructure investment is expected to be a key contributor, improving productivity and reducing operational constraints for businesses across the economy.

From an economic intelligence standpoint, the convergence of IMF-led stabilisation, AfDB-backed energy frameworks, and private capital inflows reflects a broader recalibration of Ghana's investment landscape. Rather than being viewed solely as high-risk exposures, Ghanaian energy assets are increasingly considered viable components of diversified institutional portfolios a signal of structural maturation.

For Ghana, the challenge now is execution. Regulatory clarity, currency stability, and efficient project delivery will determine the extent to which current capital inflows translate into durable economic gains. The capital is moving. The question is whether the institutional infrastructure can absorb it at the pace the economy needs. Post-IMF Ghana is not a recovery story it is a structural entry point.