The 60/40 portfolio has long been a staple for retirees, near-retirees and others with a moderate risk tolerance seeking a blend of growth and capital preservation. But 60/40 proponents were tested after 2022 when the Fed’s rapid anti-inflation rate hikes caused a simultaneous bear market in both U.S. equities (-19.4%) and bonds (-13.1%). Meanwhile, long-term U.S. Treasurys fell by over 29% and corporate bonds lost 15.7%. Some cautious investors are still recovering.

Over the past 150 years, there have been 19 bear markets for stocks, but only three bear markets for bonds. Still, a 60/40 portfolio would have resulted in 11 bear markets during those time periods—defined as negative 20% or more. With 2022 still fresh in many advisors’ and clients’ minds, it raises the question: Is a 60/40 allocation still a viable investment diversification option?

Modern portfolio theory tells us yes. Bonds and stocks are considered to have a low or negative correlation, making them effective for portfolio diversification. But let’s examine some of the important observations that investment analysts have made about the 60/40 heuristic—the traditional answer to managing risk and reward.

-

The 60/40 portfolio overlays Modern Portfolio Theory. Since being popularized by Nobel Prize-winning economist Harry Markowitz in the 1950s, MPT has been the go-to investment strategy for structuring a portfolio focused on wide diversification and performance rather than on individual stocks. MPT fundamentally changed how individuals and institutions manage investments. But MPT has faced recent criticism, particularly for its inability to account for systemic risks.

-

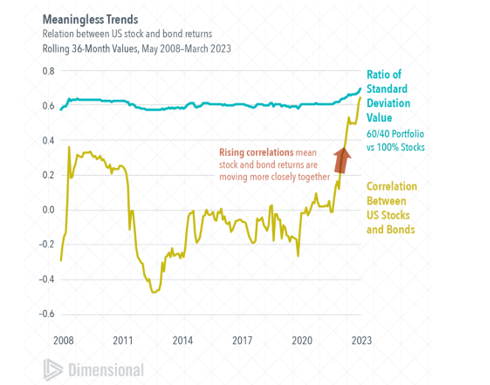

The 60/40 strategy, built on diversification using correlation coefficients, acknowledges that correlation is not constant across time. For instance, the long-term U.S. stock vs. U.S. bond correlation from 1901 through 2022 has been approximately 0.19. But if you just look at the past 15 years, the correlation has ranged from +0.6 to -0.5. (Remember, this is a scale of -1 to +1). A correlation of 0.19 is a weak, positive correlation. But there have been a strong handful of periods when the behavior of U.S, stocks vs. U.S. bonds matched 2022. For instance:

-

1916 – 1924: U.S. stocks were down 45.7% and U.S. bonds were down 45%.

-

1946 – 1950: U.S. stocks were down 25.5% and U.S. bonds were down 24%.

If this relationship held true most of the time, the 60/40 strategy would not be an effective way to diversify away risk. Fortunately, these sharp, simultaneous declines in stocks and bonds have only happened a few times.

-

Only time will tell if bonds continue to hedge portfolios during the next stock downturn. But at this juncture, there is little to no evidence that the correlation has necessarily broken.

-

Analysts predict that large caps will underperform historic norms over the next 10 years. The BoA forecast assumes that 60/40 means that large cap underperformance will lead to a bad decade of performance for this allocation. Other managers do not make the same assumption.

-

Commodity exposure is a good hedge against a weakening domestic currency. Many commodities have higher standard deviations than the 60/40 portfolio predicts. Investors can get second-order commodity exposure via the mining and refining companies in their equity mix.

-

An alternative 70/30 allocation is a consideration, but it underperforms the 60/40 allocation over long time horizons. Clients could also consider a 50/30/20 (with 20% in alternatives), but 50/30/20 has issues with direct commodity exposures.

-

Owning risky assets that are not highly correlated is how you make sure your clients are exposed to the amount of risk they purchased. Therefore, they should expect a return that will help them reach their goals. Don’t let a single random event—like the COVID-19-influenced year of 2022—lessen your belief in the long-term reliability of the 60/40. Many investors do not realize they are buying risk, but they are. Every portfolio has measurable risk based on historical data. If that risk does not align properly with the chosen allocation, they are either over- or under-exposed to the risk they are willing to accept. This is a major fault of most portfolio designs.

-

Risk tolerance is the key to any successful investment relationship. It’s critical to understand each client’s willingness to deal with the frequency and magnitude of volatility on the journey to reaching their goals.

Building a 60/40 portfolio that can withstand interest rate volatility is key to managing a portfolio. Stocks are always volatile. Bonds are designed to buffer volatility. Bonds are evaluated based on duration and the issuer’s creditworthiness. Short maturities and high creditworthiness reduce the coupon rate while also protecting fair market value when interest rates rise. The greater the yield the manager seeks from the bonds, the higher the probability of a negative impact on portfolio value. Bonds with maturities of 10, 20, and 30 years lock in higher returns but also expose the portfolio to swings in net asset value. Advisors must ensure clients understand bonds and the risks associated with them.

The 60/40 portfolio has been optimal during periods when bonds are low-risk investments with yield. So, preemptively abandoning the 60/40 allocation would be a vote of low/no confidence in the ability of U.S. institutions to service their debt. The extent to which investors question the long-term ability of the government to pay interest on the national debt may influence their willingness to hold Treasurys and other government securities.

I’ll leave you with two important considerations:

1. There is no way to predict with any degree of certainty what is going to happen in the future. But does it matter?

In the chart below, the blue line shows the ratio of trailing three-year standard deviation values for a 60% stock/40% bond allocation relative to a 100% stock allocation from May 2008 to March 2023. We see that adding fixed income to the mix reduced volatility. While the correlation was volatile, the standard deviation stayed consistently around 0.6. This means the proportional reduction in volatility through diversification was largely unrelated to the estimated correlation. Thus, recent concerns about rising positive correlations between stocks and bonds may not be a big deal for investors.

2. Managing markets has long been the most effective way to navigate volatility.

Advisors need a widely diversified portfolio of stocks and should supplement that diversity with bonds to provide additional downside protection. Getting a 0% return on bonds in a given year is painful to be sure. But 0% is preferable to significant losses caused by the mark-to-market methodology applied to long-term bonds, even if they are held to maturity.

No strategy is 100% reliable. But until I see a major breakthrough, it’s hard to argue with the success of 60/40 for clients with moderate risk tolerance who need a blend of growth and capital preservation to reach their goals and sleep soundly at night.

{kind=link}