- 12-month outlook improves

- Employment increases for the fifteenth successive month

- Data were collected 10-23 May 2024

Doha, Qatar – The upturn in Qatar’s non-energy private sector gained notable momentum in May, according to the latest Purchasing Managers’ Index™ (PMI®) survey data from Qatar Financial Centre (QFC) compiled by S&P Global. Output and new orders increased at the fastest rates since the third quarter of 2023, companies continued to expand employment and the 12-month outlook improved. Inflationary pressures remained muted, with input prices broadly unchanged and output charges up only modestly since April.

The Qatar PMI indices are compiled from survey responses from a panel of around 450 private sector companies. The panel covers the manufacturing, construction, wholesale, retail, and services sectors, and reflects the structure of the non-energy economy according to official national accounts data.

The headline Qatar Financial Centre PMI is a composite single-figure indicator of non-energy private sector performance. It is derived from indicators for new orders, output, employment, suppliers’ delivery times and stocks of purchases.

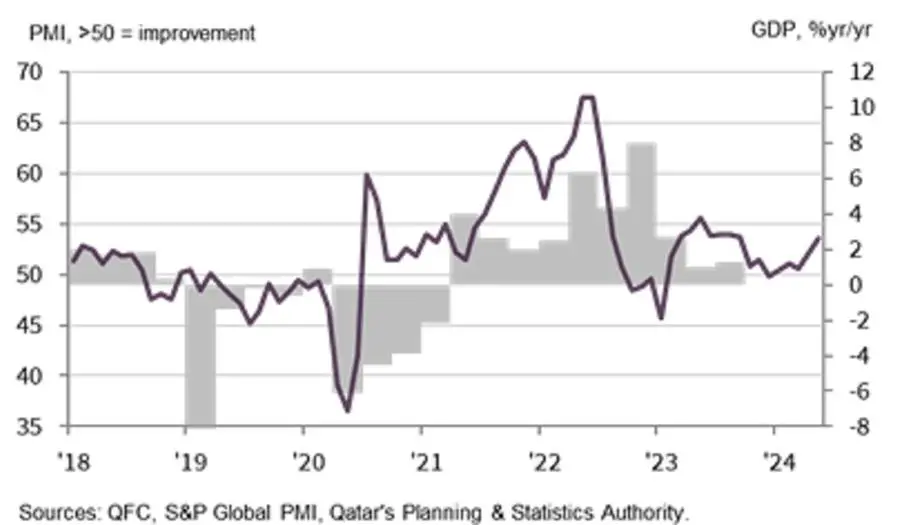

The PMI registered 53.6 in May, up from 52.0 in April, rising further above the no-change mark of 50.0 and signalling the strongest improvement in business conditions in the non-energy private sector economy since last September. It was also above the long-run trend level of 52.3 (since April 2017). The 1.6-point increase in the PMI was among the largest registered over the past two years.

May data signalled growing demand momentum in the non-energy economy. The level of incoming new work expanded at the sharpest rate in eight months, and faster than the long-run survey trend. Companies often mentioned that their reputations for high-quality products and services had attracted new clients.

The accelerated increase in new business wins in May generated the fastest growth in total business activity since last August. All four broad sectors posted quicker expansions, led again by wholesale & retail and services. Although new business growth strengthened, companies were still able to reduce the volume of outstanding work during the month.

Confidence regarding the next 12 months strengthened in May. Increasing optimism among non-energy private sector companies was linked to development plans and marketing campaigns, plus the introduction of new high-quality products and services.

Faster growth of output and new orders was reflected in another increase in employment. Hiring activity was linked to company development goals, including efforts to speed up the delivery of high-quality services and to gain staff experienced in new technologies.

Demand for inputs rose in May, as purchasing activity increased at the second-fastest rate in ten months. Lead times continued to improve, however, as firms reported building supplier relationships. Input stocks fell for the fifth time in six months as output growth accelerated.

Cost pressures were broadly stable as average purchase prices declined, offsetting higher wages. Prices charged for goods and services increased for the second time in the past seven months, but at a slower rate than the previous hike in March.

QFC Qatar PMI vs. GDP

Financial Services

Growth in financial services activity surges in May

- Steepest increases in total activity since May 2023

- New business inflows and 12-month outlook both strengthen

- Charges for financial services broadly stable

Qatari financial services companies recorded much faster growth in volumes of total business activity and new contracts in May. The seasonally adjusted Financial Services Business Activity and New Business Indexes rose to 12- and eight-month highs of 60.9 and 59.1, respectively, well above the equivalent indices for the non-energy private sector as a whole.

Companies were also increasingly optimistic regarding the 12-month outlook, with confidence the highest since last July 2023. Meanwhile, employment growth was maintained for the fourteenth successive month.

In terms of prices, average charges set by financial services companies were broadly unchanged since April, following a four-month sequence of discounting. Meanwhile, average input prices rose slightly and for the first time in three months.

Comment

Yousuf Mohamed Al-Jaida, Chief Executive Officer, QFC Authority:

“The May results clearly indicate that the non-energy private sector has moved up a gear as we approach the halfway point of 2024. Growth rates for output and new orders accelerated notably, and companies became more optimistic regarding the next 12 months.

“Both the wholesale and retail and the services sectors continued to drive expansion in May, and financial services remained a bright spot.

“Although there was a rise in output prices in May, inflationary pressures broadly remained in check and suppliers’ delivery times continued to improve.”

-Ends-

ABOUT THE QATAR FINANCIAL CENTRE

The Qatar Financial Centre (QFC) is an onshore business and financial centre located in Doha, providing an excellent platform for firms to do business in Qatar and the region. The QFC offers its own legal, regulatory, tax and business environment, which allows up to 100% foreign ownership, 100% repatriation of profits, and charges a competitive rate of 10% corporate tax on locally sourced profits.

The QFC welcomes a broad range of financial and non-financial services firms.

For more information about the permitted activities and the benefits of setting up in the QFC, please visit qfc.qa

@QFCAuthority | #QFCMeansBusiness@QFCAuthority | #QFCMeansBusiness

MEDIA CONTACTS

QFC: Rasha Kamaleddine, Marketing & Corporate Communications Department, r.kamaleddine@qfc.qa

ENQUIRIES ABOUT THE REPORT

QFC: qatarpmi@qfc.qa

ABOUT S&P GLOBAL

S&P Global (NYSE: SPGI) S&P Global provides essential intelligence. We enable governments, businesses and individuals with the right data, expertise, and connected technology so that they can make decisions with conviction. From helping our customers assess new investments to guiding them through ESG and energy transition across supply chains, we unlock new opportunities, solve challenges, and accelerate progress for the world.

We are widely sought after by many of the world’s leading organizations to provide credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity, and automotive markets. With every one of our offerings, we help the world’s leading organizations plan for tomorrow, today. www.spglobal.com.

ABOUT PMI

Purchasing Managers’ Index™ (PMI®) surveys are now available for over 40 countries and for key regions including the Eurozone. They are the most closely watched business surveys in the world, favoured by central banks, financial markets and business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends.

www.spglobal.com/marketintelligence/en/mi/products/pmi.html

METHODOLOGY

The Qatar Financial Centre PMI® is compiled by S&P Global from responses to questionnaires sent to purchasing managers in a panel of around 450 private sector companies. The panel is stratified by detailed sector and company workforce size, based on contributions to GDP. The sectors covered by the survey include manufacturing, construction, wholesale, retail, and services.

Survey responses are collected in the second half of each month and indicate the direction of change compared to the previous month. A diffusion index is calculated for each survey variable. The index is the sum of the percentage of ‘higher’ responses and half the percentage of ‘unchanged’ responses. The indices vary between 0 and 100, with a reading above 50 indicating an overall increase compared to the previous month, and below 50 an overall decrease. The indices are then seasonally adjusted.

The headline figure is the Purchasing Managers’ Index™ (PMI). The PMI is a weighted average of the following five indices: New Orders (30%), Output (25%), Employment (20%), Suppliers’ Delivery Times (15%) and Stocks of Purchases (10%). For the PMI calculation the Suppliers’ Delivery Times Index is inverted so that it moves in a comparable direction to the other indices.

Underlying survey data are not revised after publication, but seasonal adjustment factors may be revised from time to time as appropriate which will affect the seasonally adjusted data series.

Data were collected 10-23 May 2024.

For further information on the PMI survey methodology, please contact economics@spglobal.com.

CONTACT

S&P Global: Sabrina Mayeen | E. Sabrina.mayeen@spglobal.com

{kind=link}