Africa’s payment landscape is undergoing a rapid and dramatic transformation, fueled by the continued rise of mobile money, the acceleration of alternative payments, and advancements in infrastructure modernization efforts, a new research by Afridigest, commissioned by Zone Network, says.

These trends are driving greater efficiency, inclusivity, and economic opportunity across the continent’s ecosystem.

The critical role of mobile money

The report, released in July, looks at the state of the payment landscape in Africa, highlighting the key trends and developments shaping the sector. In particular, it notes the dynamic payment ecosystem of Africa that’s characterized by an hybrid transformation most visible in mobile money.

Mobile money is a digital financial service that allows people to store, send, and receive money using a mobile phone, without needing a traditional bank account. It typically works through a mobile network operator or a specialized financial service provider, often via simple text-based USSD codes or mobile apps. These services also operate with extensive agent networks, which serve as hubs for distribution, liquidity, and customer service, enabling scale, and adoption in places where formal banking infrastructure is scarce.

This hybrid model has allowed mobile money to expand financial access for millions previously excluded from the formal banking system, and significantly contribute to economic growth.

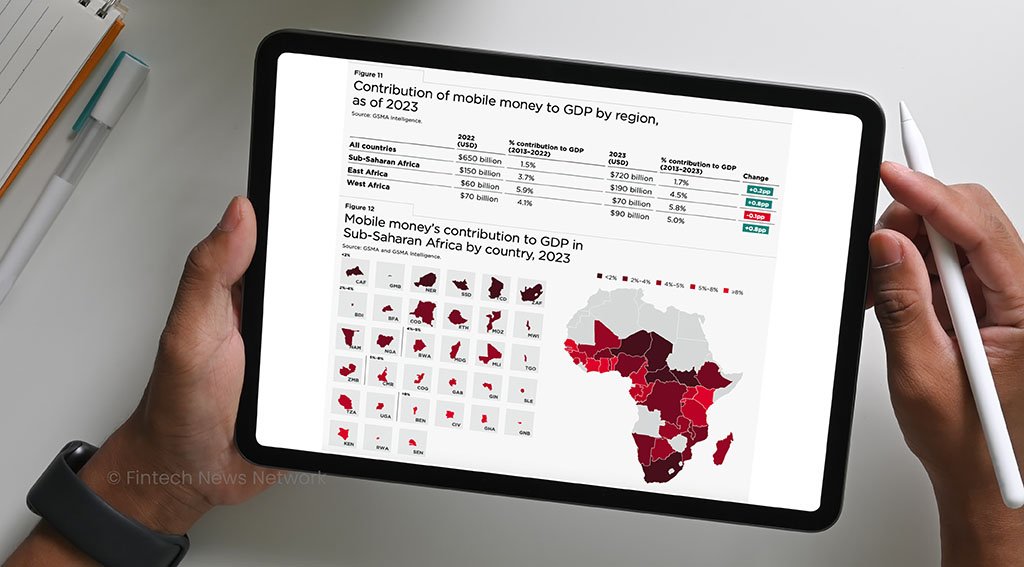

In 2023, mobile money contributed 4.5% to Sub-Saharan Africa’s GDP, with some countries such as Senegal, Rwanda, and Kenya surpassing 8%, according to the Global System for Mobile Communications Association (GSMA). Globally, that share stood at just 1.7%, reflecting the more profound economically impact of mobile money in Africa.

Last year, mobile money counted over 500 billion monthly active users and 2 billion total registered accounts. Africa remained at the epicenter of this industry, posting 1.1 billion registered mobile money accounts, and processing US$1.1 trillion, equivalent to more than US$2 million a minute.

Comprehensive finance platforms

With mobile money continuing to gain ground, these providers have started expanding their platforms into comprehensive financial ecosystems to create new revenue streams, and improve customer retention. These platforms now integrate with banks, fintechs, and global payment networks, offering services ranging from e-commerce payments and credit, to insurance and enterprise solutions for micro, small, and medium-sized enterprises (MSMEs).

In Kenya, for example, M-Pesa has expanded from P2P transfers to bill payments, savings, investments, loans, buy now, pay later (BNPL) offerings, virtual cards, and insurance through strategic partnerships. Similarly, in South Africa, MTN MoMo now offers products and services across payments, e-commerce, insurance, lending, and remittances.

Agent networks have also expanded beyond financial services entirely, becoming crucial last-mile distribution channels for e-commerce, government services, and more.

In Egypt, for example, Brimore connects small and medium-sized manufacturers to the mass market via a network of distribution agents, most of whom are women. These agents handle the marketing, sales, and distribution of the products.

In Rwanda, Irembo offers over 100 e-government servicesaccessible via online portals, USSD, and support agents.

The rise of alternative payments

Africa is also seeing rapid growth in alternative payment methods, including account-to-account (A2A) payments, digital wallets, QR code payments, and cryptocurrencies.

A key driver of this shift is the rise of instant payment systems, which enable real-time A2A transfers. As of mid-2024, 28 domestic instant payment systems operated across 20 African countries, with 31 more under development.

In Africa, real-time payment rails are fueling the rise of digital payments. In Nigeria, for example, the NIBBS Instant Payment (NIP), launched in 2011, accounted for 82.1% of all cashless transactions in 2023, according to paytech firm ACI Worldwide. In 2023, 27.7% of transactions in the country were made using real-time payments, but by 2028, this is expected to increase to 50.1%.

Real-time payment systems are also driving innovation, with fintech startups, telecom giants, and traditional banks leveraging this infrastructure to offer innovative solutions.

In Nigeria, payment gateways like Paystack are supporting instant payment transfers to boost transaction conversion rates and settlement speeds.

Neobanking platforms and super-apps such as Kuda, and Moniepoint are integrating real-time payments for consumer P2P and merchant QR code payment with know-your-customer (KYC), savings, credit, and other value added services to improve customer experience.

Interoperability and cross-border payments

Another key trend driving the payment landscape is Africa is the rapid growth of cross-border interoperability.

The Pan-African Payment and Settlement System (PAPSS) is at the heart of this shift. Launched in 2022 by the African Union (AU) and the African Export-Import Bank (Afreximbank), the system enables instant cross-border payments in local currencies, eliminating the need to convert to US dollars for intra-African transactions and potentially saving the continent over US$5 billion annually in transaction costs. It aims to promote financial inclusion and boost intra-African trade under the African Continental Free Trade Area (AfCFTA), fostering a more integrated and self-sustaining African economy.

PAPSS covers most African countries and works in collaboration with central banks to provide a payment and settlement service to which commercial banks and licensed payment service providers across the region can connect.

Adding to the PAPSS system, the consortium launched in June 2025 PAPSSCARD, the continent’s first Pan-African card scheme.

Beyond public initiatives, private-sector innovation is also accelerating connectivity between Africa and the world. A prime example of this is Nigeria’s Zone, which has developed Africa’s first regulated blockchain network for payments.

Licensed by the Central Bank of Nigeria, Zone employs decentralized P2P architecture that connects banks and fintech companies in the country. This allows transactions to be processed directly between participating institutions without dependence on intermediaries, solving critical industry challenges such as painful reconciliation processes, slow settlement times, and high failure rates.

Digital currencies, particularly stablecoins, are another transformative force in cross-border payments. They promise to further reduce friction, cost, and risk in cross-border transactions, with several Africa-focused initiatives already underway.

Africa’s digital payment landscape is expanding at an unprecedented rate. McKinsey estimates that the continent’s cashless payments industry will grow by more than 150% between 2020 and 2025, surging from US$15 billion in revenue to almost US$40 billion from domestic payments alone.

Featured image: Edited by Fintech News Africa, based on image by sodawhiskey via Freepik

{kind=link}