While the fintech sector in Nigeria has grown markedly over the past years, stakeholders still face persistent obstacles that impede their growth, including regulatory uncertainty, infrastructure deficiencies, and compliance costs, according to a new report by the Central Bank of Nigeria (CBN).

The report, based on a 2025 survey of leading fintech executives, a closed‑door workshop held in June, and the CBN Fintech Roundtable in October, shares the challenges faced by the industry, highlighting that regulatory clarity and the speed of decision‑making are the most consistent concerns for stakeholders.

62.5% of surveyed respondents cited delays in approvals and ambiguity in regulatory guidelines as the chief constraints on product development and innovation timelines, with 37.5% of respondents reporting that it can take over a year to bring new products to market.

Fintech regulation advances but challenges remain

Compliance-related expenditure also weigh heavily on innovation capacity. 87.5% of the surveyed stakeholders indicated that costs tied to fraud controls, cybersecurity investments, and anti-money laundering and countering the financing of terrorism (AML/CFT) infrastructure significantly affect their operations.

Overall, half of the participants described the regulatory environment as supportive to fintech innovation, while the other half viewed it as restrictive. This underscores a split perception of progress versus remaining gaps.

Stakeholders advocated for a centralized channel to streamline engagement across multiple regulatory domains. This is particularly relevant considering that fintech innovations can have a cross-sectoral impact.

Among those surveyed, 62.5% supported this proposal, emphasizing the desire for simplified and efficient supervisory engagement. These supporters believe such a mechanism can reduce friction, accelerate time‑to‑market, and improve coordination across governmental agencies.

Technology and infrastructure gaps

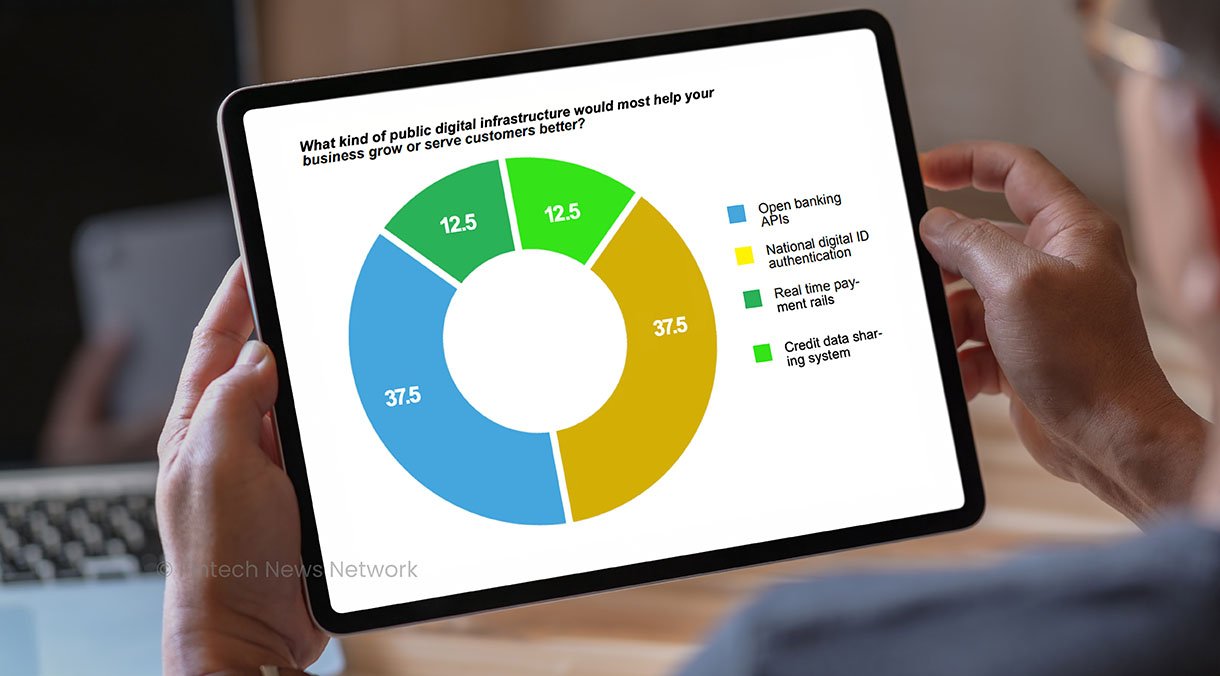

Fintech stakeholders also pointed to several infrastructure shortcomings that are hindering development. They emphasized the lack of universal access to digital identity verification, limited broadband penetration, incomplete data-sharing systems, and limited open-data frameworks as key barriers.

Stakeholders stated that while digital identity systems exist in Nigeria, fragmentation and integration gaps diminish their effectiveness. 37.5% of surveyed respondents identified a national digital ID authentication system as a priority for growth.

An equal share (37.5 %) highlighted the need for robust open banking interfaces to facilitate seamless data exchange. Respondents shared that fragmented APIs, inconsistent data-sharing protocols, and a lack of universal service standards are making integration across platforms challenging.

The need for regulatory passporting

Nigerian fintech stakeholders view regional expansion as essential for achieving scale and success, with 62.5% of respondents either already operating or planning to operate across other African markets.

Hence, the same proportion of respondents support a regulatory passporting framework that would enable mutual recognition of licenses. Such a framework would remove the administrative and regulatory hurdles that typically accompany cross‑border operations by allowing a license granted in one jurisdiction to be recognized in others.

Ghana, Kenya, South Africa, Uganda, and Senegal were named as the most suitable countries for piloting the proposed model.

Stakeholders also showed interest in bilateral collaborations on technical infrastructure. This includes, for example, trialing interoperability between Nigeria’s and Ghana’s payments systems to enhance cross-border payments and support real-time regional settlement.

Regulating cryptocurrencies

The study also looked at the cryptocurrency sector, with stakeholders emphasizing the potential of digital currencies to drive cost-effective cross-border transactions, increase financial inclusion, and catalyze new digital asset markets. However, there was equally strong acknowledgement of the risks, particularly around illicit flows, speculative bubbles, and consumer protection.

Participants broadly agreed on the need for a risk-based, activity-focused regulatory framework, calling for clarity on permissible activities for licensed institutions, consumer advisories on volatility and fraud, and strengthened international collaboration on AML/CFT compliance and information sharing. Stakeholders also advised for the establishment of sandbox tracks to explore relevant use cases in Nigeria, such as remittances, capital markets, and central bank digital currencies (CBDCs).

AI adoption of the rise

The research also addressed the use of artificial intelligence (AI) in the Nigerian fintech sector. It found that AI is widely adopted among Nigerian fintech companies, especially for risk management and operational efficiency.

87.5% of the companies surveyed were either using or exploring the use of AI for fraud detection, underscoring the severity of the fraud challenge, which was described in the closed-door stakeholder workshop as a “big issue in the industry”. Chatbots and customer service were another key AI use case, cited by 62.5% of respondents. Other key use cases included credit scoring and risk modeling (37.5%) and customer onboarding/KYC (37.5%).

Despite the enthusiasm for AI, fintech companies from Nigeria face a number of challenges. When asked what support their organizations need to adopt or scale responsible AI innovation, 50% cited access to high quality data infrastructure, and 25% pointed to pilot partnerships with regulators or research institutions.

These results indicate that without robust data foundations, even the most advanced AI models cannot be trained or scaled effectively. They also show that collaboration with regulators and academics is critical to shape ethical and compliant AI solutions.

The Nigerian fintech industry has grown tremendously over the past decade, now boasting over 500 startups. However, most of this activity concentrates in payments, leaving major gaps and opportunities in categories including insurtech and fintech infrastructure.

Featured image by thanyakij-12 on Freepik

{kind=link}