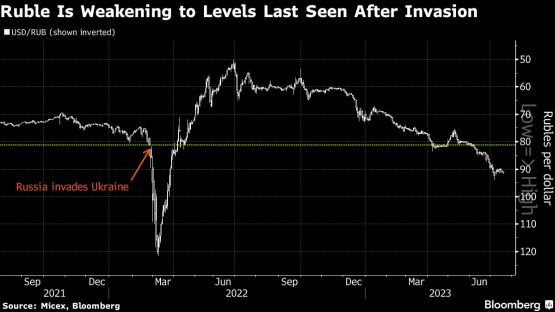

Russia is poised for its first interest-rate hike since emergency measures taken after the invasion of Ukraine almost 17 months ago, as a stretch of steep currency depreciation forces the central bank’s hand.

A failed mutiny in June has thrust the ruble into the spotlight by adding to pressure from a deterioration in foreign trade that’s turned it into one of the worst performers this year in emerging markets against the dollar. Three-month implied volatility for the currency, a gauge of anticipated moves, is also the world’s highest.

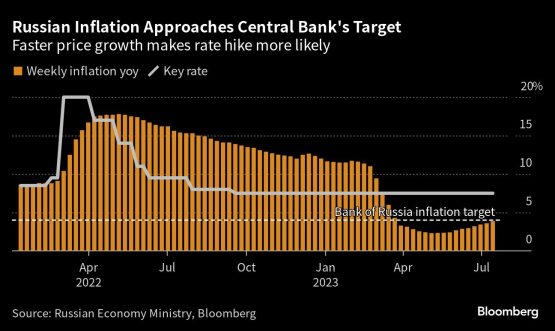

A weaker ruble is accelerating the timeline for monetary tightening after months of warnings by the central bank that higher rates were on the way in response to inflationary risks from heavy government spending, sanctions and labour shortages caused by the call-up of men to fight in Ukraine.

Almost all economists surveyed by Bloomberg expect policymakers to act on Friday, with forecasts ranging between a hike of 25 and 75 basis points. Goldman Sachs Group is the lone dissenter predicting the benchmark will stay at 7.5%.

“The ruble selloff necessitates a new tightening cycle,” said Tatiana Orlova of Oxford Economics.

“The mutiny may have indirectly contributed to the selloff by affecting exporters’ choice of whether to sell export proceeds on the local market or hold on to them, or intensifying capital flight via other channels,” Orlova said.

The armed rebellion by Wagner mercenaries that briefly threatened President Vladimir Putin’s power carries the risk of triggering further outflows of money at a time when falling energy earnings and a recovery in imports drain the economy of hard currency.

It’s a prospect that could be a drag on the ruble in the months to come. The Russian currency has already lost about 18% this year, with more than a third of the depreciation coming after Wagner’s attempted march to Moscow.

Though Bank of Russia Governor Elvira Nabiullina has called the ruble’s floating exchange rate “a blessing” for the economy, the currency’s retreat is making imports more expensive as annual price growth approaches the central bank’s 4% target.

Inflation expectations for the next 12 months — a key concern for the central bank — exceeded 11% in July with the sharpest increase in almost a year.

What Bloomberg Economics Says…

“The central bank’s guidance is expected to be hawkish and suggest further hikes are on the table at the next meeting in September. We expect the central bank’s rhetoric to become more hawkish or moderate, depending on whether year-on-year growth in public spending accelerates or slows from the 20% reported for the first six months of 2023.”

—Alexander Isakov, Russia economist.

A decision to lift rates would end the longest pause in more than seven years by the central bank, which hasn’t adjusted rates since six rounds of easing ended in September. It last hiked the benchmark days after the invasion with an emergency increase to 20%, the highest in almost two decades, as unprecedented international sanctions battered Russia’s economy and assets.

Given the uncertainty around inflation and the exchange rate, investors have recently dumped ruble government bonds in anticipation of a policy pivot.

Price pressures are set to remain elevated for most of the second half of this year, creating a window for further increases at the next three policy meetings, according to Sofya Donets, an economist at Renaissance Capital.

“The acceleration of price growth amid the unexpected scale of the ruble’s weakening has made a rate hike inevitable,” Donets said in a note.

© 2023 Bloomberg

{kind=link}