Due to higher technology demands, inflation concerns and rising geopolitical uncertainty, investors are increasingly seeking hard assets for peace of mind.

Assets such as gold, silver, platinum, palladium and other precious metals have seen increased demand, and their prices have risen to near-record levels over the last year. For instance, gold appreciated a whopping 65% in 2025, and silver appreciated 144%! Even with the recent sell-off, gold and silver gained approximately 13% and 19% respectively in January 2026.

With precious metals prices at such frothy levels, many of your clients may be anxious to sell precious metal assets to raise cash or to rebalance their portfolios. But taxes need to be factored into that decision.

Collectibles Classification and Applicable Rates

Gold, silver and most other precious metals and non-U.S.-minted coins held for investment are classified as “collectibles” under Internal Revenue Code Section 408(m). They’re not securities. Short-term gains from sales of collectibles are taxed at the taxpayer’s ordinary income rates. Long-term (held for over one year) gains are subject to a maximum federal rate of 28%.

This 28% rate serves as a ceiling. Taxpayers in lower tax brackets will pay a lower rate, while higher-income taxpayers are limited to the 28% maximum on long-term collectible gains. However, there are limited exceptions under IRC Section 408(m)(3) to the “collectibles” definition for certain U.S.-minted coins held by individual retirement accounts, including:

-

Gold coins described in 31 USC Section 5112(a)(7)-(10) are the American Gold Eagle coins. These coins are issued in denominations of $50 (containing one ounce of fine gold), $25 (1/2 ounce), $10 (1/4 ounce), and $5 (1/10 ounce)

-

Silver coins described in 31 USC Section 5112(e) are American Silver Eagles. These are one-dollar coins containing one troy ounce of .999 fine silver, produced by the U.S. Mint as legal tender

-

Platinum coins described in 31 USC Section 5112(k)

-

Coins issued by any U.S. state

These coins would be taxed at a 20% or lower capital gains rate, depending on the taxpayer’s adjusted gross income (AGI) at the time the IRA distributes the gain. Interestingly, the premium an investor will pay for U.S.-minted coins is much less than the potential tax rate savings. Thus, higher-income taxpayers who own U.S.-minted coins held in an IRA should always try to invest in U.S. coins rather than foreign coins such as Maple Leafs, Pandas and Krugerrands.

In addition to income taxes, higher-income individuals may owe the 3.8% net investment income tax (NIIT) if their modified AGI is over $200,000 single or $250,000 married filing jointly.

Accounting Method’s Effect on Gain

The Internal Revenue Service allows taxpayers to use the specific identification method to determine the cost basis when selling precious metals if the metals can be adequately identified. With current prices near record highs, using the specific identification method to sell recently acquired items first can help taxpayers minimize taxable gains on these metals.

Coins and Bullion Received as a Gift vs. Inheritance

If your client received gold as a gift, their cost basis is generally tied to the donor’s original purchase price, not its value at the time they received it. This can dramatically raise their tax hit on sale. If the gold came through an inheritance, however, it will usually receive a step-up in basis to its fair market value at the time of the original owner’s death.

As the old saying goes, “What goes up must come down,” and we saw the biggest drop in gold and silver on Friday Jan.30, 2026. Gold dropped 8.97%, and silver dropped 25.97% over the trading day. The sell-off continued early into the following week.

To make lemonade out of lemons, taxpayers can consider selling off any coins or bullion that have dropped below their cost basis and claim a tax loss. They can then immediately repurchase the same or other metals without concern for IRC Section 1091, which disallows losses on “wash sales” of stock or securities. That’s because physical gold, silver and other precious metals aren’t subject to this rule. Crypto is also exempt from the wash sale rules for now.

Sales Tax

Unlike sales of securities, many municipalities and some states impose sales tax on the purchase of precious metals. Each state is different. For more information about sales tax in your state, see Swiss America’s state guide on precious metals sales tax: Sales Tax On Gold And Silver By State: 2026 Guide (Swiss America blog, January 8, 2026).

Tax Deferral Opportunities

In certain circumstances, taxpayers may be able to defer recognition of taxable gains from the sale of precious metals through strategic planning. From a planning perspective, taxpayers may consider timing sales, using capital losses to offset gains.

Clients with capital gains exceeding $100,000 may want to consider deferring the gain under the federal opportunity zone program. Similar to a IRC Section 1031 transaction, clients can roll their gains within 180 days of the sale date and defer taxes for up to five years.

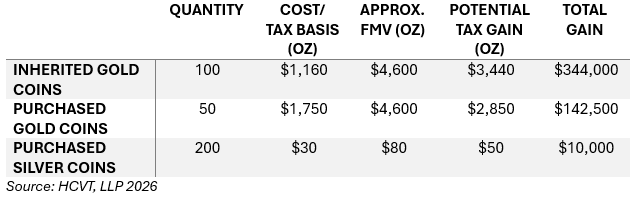

Real World Example

To illustrate, Client X inherited his father’s coin collection in 2015. Since then, he’s periodically purchased additional U.S. Mint gold and silver coins.

In total he owns:

If Client X sold 50 gold coins, their taxable gain would be $29,500 lower (50 x $590 basis difference) by simply selling their more recently purchased coins first, rather than selling the lower basis inherited coins.

If Client X sells all the non-inherited coins, their tax gain will be approximately $152,500 based on recent spot prices. Note that coins issued by the U.S. Mint (and other foreign mints) typically trade at a premium compared to “blanks” (non-legal coins) and bullion, averaging approximately $8 to $10 per ounce for silver and 5% to 8% for gold.

Although Client X is eager to capitalize on the recent surge in precious metal prices, they are understandably less enthusiastic about the tax consequences that accompany a sizable tax gain. We reviewed the option of deferring recognition by reinvesting the gain into a captive qualified opportunity zone (OZ) fund within 180 days of the sale. This approach allowed Client X to redirect proceeds into real estate or an operating business while postponing current tax and potentially building up tax-free gains, provided that the OZ investment is held for at least ten years and all statutory requirements are met.

Avoid Unexpected Consequences

Although gold and silver are commonly viewed as safe stores of value, their tax treatment is more complex than that of traditional securities. Physical precious metals and many bullion-backed exchange-traded funds are classified as collectibles, subjecting long-term gains to a higher maximum federal rate of 28%, with potential exposure to the NIIT and state taxes.

Given the recent dramatic price movements and increased investor activity, make sure clients are aware of these rules to avoid unexpected tax consequences.

The author acknowledges Kaitlynn Robertson and Emily Cook, tax interns in the Salt Lake City office of HCVT, for their help with this article.

{kind=link}