Rising oil prices linked to current tensions in the Middle East could significantly raise mining costs and pressure sector margins, according to a new BMO Capital Markets report.

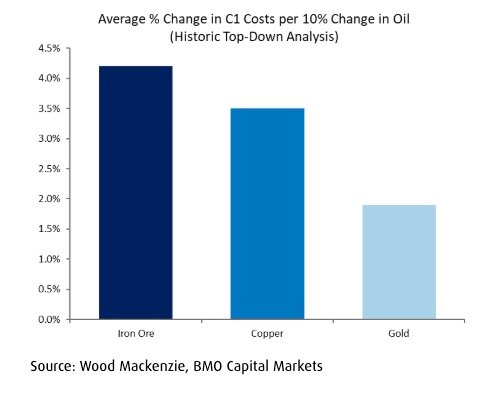

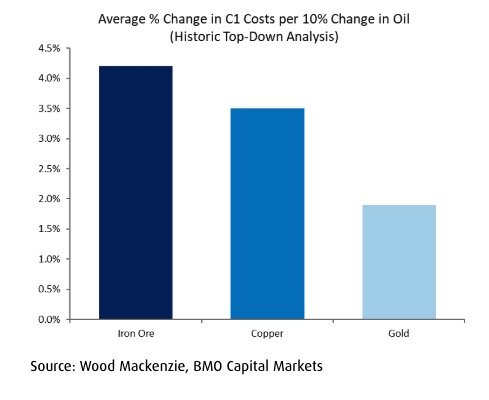

Examining historical cost trends using Wood Mackenzie data, analysts found mining expenses rise sharply with crude prices, though exposure varies by commodity. Iron ore operations are the most sensitive, with costs increasing about 4.2% for every 10% rise in oil prices, compared with roughly 3.5% for copper and about 2% for gold. If crude averages about $100 a barrel — around 47% above the 2025 average — mining costs could climb roughly 20% for iron ore, 16% for copper and 9% for gold.

Looking back over the last roughly 25 years, BMO sees iron ore (4.2%), copper (3.5%) and then gold (1.9%) facing the greatest cost sensitivity to oil price changes

Brent crude prices held above $100 a barrel on Friday even after the United States temporarily eased sanctions on Russian oil. The licence, posted on the U.S. Treasury website, applies only to Russian crude and petroleum products loaded onto vessels as of March 12 and allows those shipments to proceed until April 11.

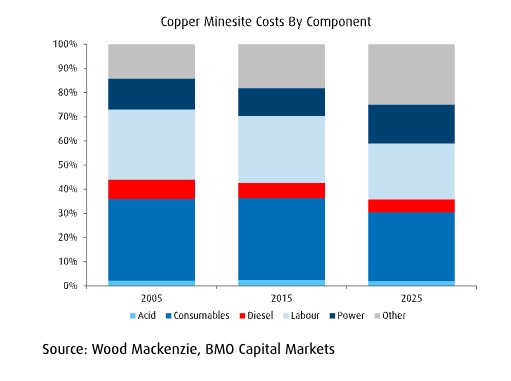

“Bottom-up” cost breakdowns often underestimate the impact because they focus narrowly on direct fuel use, analysts said. Diesel accounts for only about 5% of copper mine operating costs today, down from roughly 8% two decades ago, but higher energy prices eventually ripple through electricity, consumables, labour and equipment, amplifying overall cost pressures.

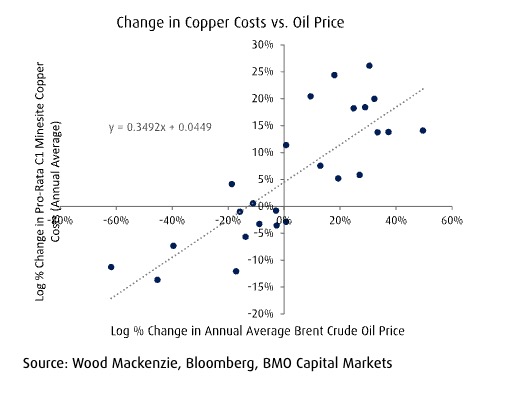

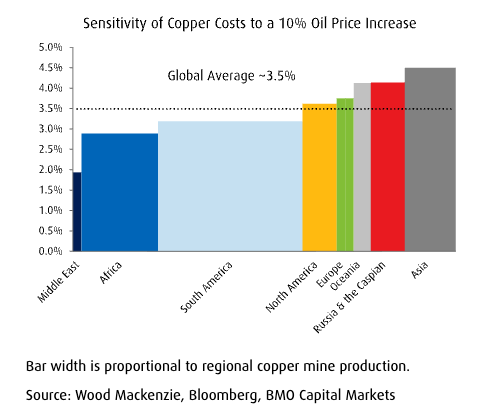

If oil prices jump by 10%, copper costs increase about 3.5%

The findings underscore how energy shocks can reshape mining economics. Sustained oil price increases not only raise operating expenses but can also shift industry cost curves, potentially altering which assets remain competitive if fuel prices stay elevated.

Regional differences

Regional exposure varies. Mines in Africa and the Americas historically show lower sensitivity to global oil prices than operations in Europe and Asia, likely reflecting access to cheaper local fuel supplies and power sources. At the same time, the industry’s vulnerability to oil has gradually declined as companies invest in fuel efficiency, electrification and captive power generation.

Diesel alone accounts for about 5% of site costs directly, down from 8% in 2005.

Supply chain risks tied to the Middle East add another layer of uncertainty. Higher sulphur prices could raise costs for copper solvent extraction and electrowinning operations that rely heavily on sulphuric acid. Meanwhile, ammonia exports —about one-fifth of which pass through the Strait of Hormuz— are a key feedstock for ammonium nitrate used in mining explosives.

The war has created the “largest supply disruption” in history, the International Energy Agency said, even as dozens of countries agreed to release 400 million barrels from strategic reserves to stabilize markets.

Across regions, Africa and the Americas look relatively more insulated than Europe and Asia.

Individual mines may experience different outcomes depending on energy hedging programs, power contracts or local supply arrangements that could delay or soften the transmission of higher oil prices into operating costs.

Still, history suggests sustained energy shocks tend to filter through the entire mining value chain, reinforcing the industry’s vulnerability to geopolitical disruptions in global fuel markets.

{kind=link}