Roach said he will be paying close attention to whether the risks between growth and inflation remain in balance.

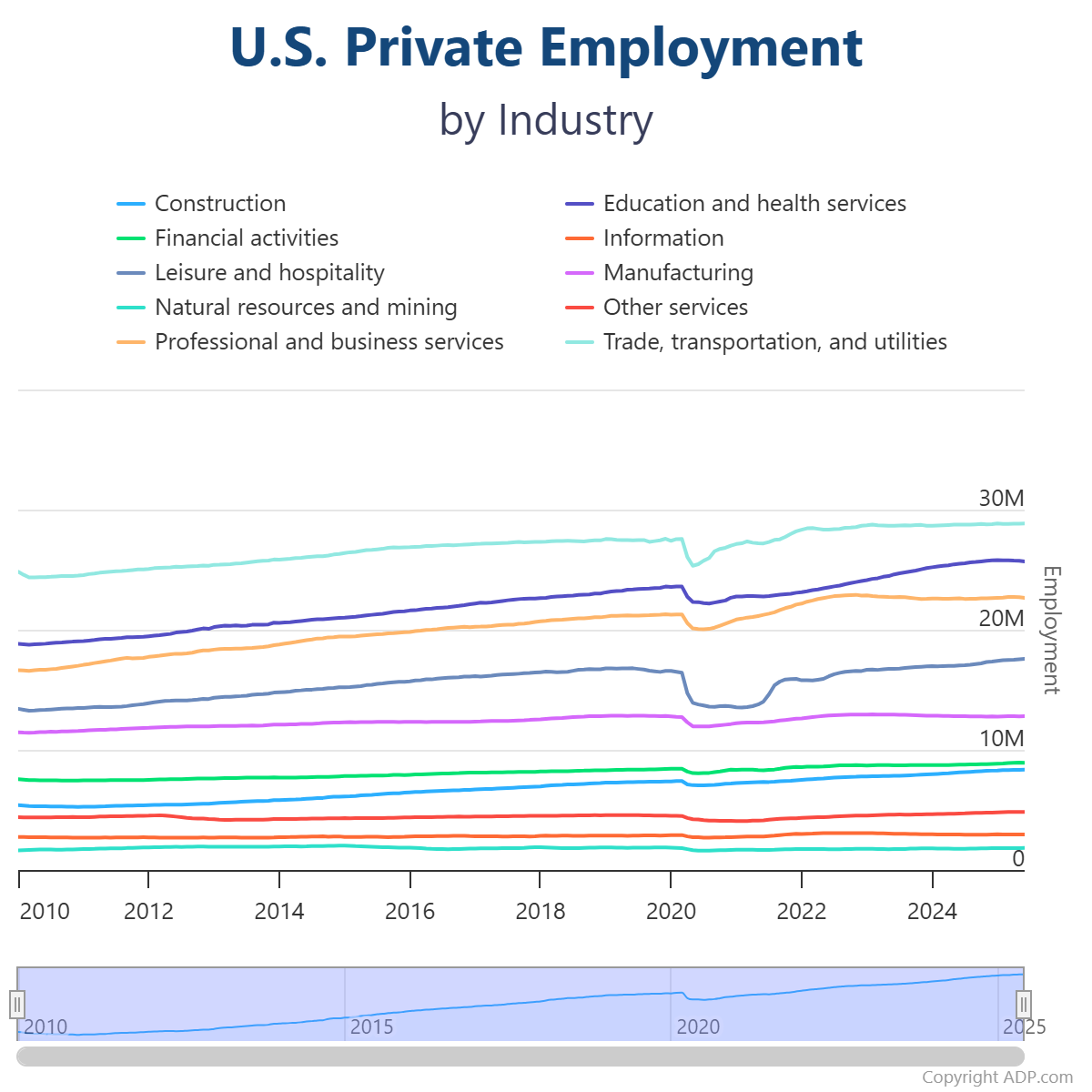

This morning’s ADP report revealed an unexpected contraction in the month of June. According to the report, private employers reduced headcount by 33,000 last month. While leisure, hospitality, and manufacturing all showed signs of improvement, professional and business services, as well as education and health services, fueled the decline overall.

Nela Richardson, ADP’s chief economist, said, “though layoffs continue to be rare, a hesitancy to hire and a reluctance to replace departing workers led to job losses last month. Still, the slowdown in hiring has yet to disrupt pay growth.”

Notable from the report is the majority of losses came from small businesses as defined by those with 19 or fewer employees, which saw their employment shrink by 29,000. Meanwhile, large establishments with 500 or more employees, added 30,000 jobs, according to the report.

The services sector, according to LPL Financial’s chief economist Jeffrey Roach, is what makes him most nervous.

“The services part of the economy is really the vast majority economy. And so looking at those areas suggest this the professional services that have had some strength in the last year or so, like leisure hospitality, restaurants, hotels – that’s been driving some of the gains over the last year,” Roach told InvestmentNews.

However, even with these weaknesses cropping up, Roach said, “I think there’s still a chance that we get the so-called ‘soft landing’ … the labor market does seem to be slowing at a fairly measured pace, and you could argue that this is one of the very few things that have been somewhat measured, given the fact that we have a ‘shock and awe’ strategy when it comes to trade policy, tax policy, and many other policies.”

President Donald Trump has spoken candidly about his critiques toward Fed chair Jerome Powell and his reticence to lower interest rates. Whether this lower-than-expected ADP report correlates to the BLS’s employment report, set to be released Thursday morning, remains to be seen. A second soft number could trigger the Fed to respond.

“I think if you get a really weak number tomorrow, I think it is going to be a catalyst for more policymakers to start talking about, ‘okay, we think that we should be focused a little bit more on the downside risk to growth.’ At this point, the consensus view is those risks between growth and inflation are roughly in balance. I think we’re probably going to be at the point where that will flip,” Roach said.

All eyes will be on the report tomorrow, and Roach said he is paying particular attention to hours worked. “I think we’re in this really unusual time period now, in 2025 where businesses had a difficult time finding qualified workers post pandemic. There is this labor hoarding going on,” Roach said. “I think what businesses might do is, instead of shedding payrolls, they might just say, well, let’s cut back hours worked to manage through the slowdown.”

{kind=link}