Eric Ludwig, left, from The American College Center for Retirement Income, and Mohan Gurupackiam, of Steward Partners.

Financial advisors are educating themselves on the potential uses of AI. Here’s how they are approaching what could very well be a game-changing technology

Financial advisors are finally smartening up about the benefits of artificial intelligence.

Managing money for a living revolves around risk management, which is why wealth managers tend to be highly risk averse. Hang around the financial services industry for a while and one will clearly discern that long-term success tends to be achieved by those practitioners who are cautious in their choices, whether they relate to an investment strategy or the latest office technology.

Seriously, do you think Warren Buffett has lasted six decades as the world’s greatest investor by day-trading IPOs and relying on the latest stock-picking software to manage his portfolio? Or did he grow Berkshire Hathaway into a $1 trillion-plus financial services behemoth by buying and holding blue chips, while sticking to his time-tested investing strategy of chugging Cherry Cokes and reading annual reports?

It’s quite clear that those perennially looking to go all in on the new, new thing (remember that gem of a phrase from the dotcom boom/bust?) don’t tend to last long on Wall Street. And that’s probably the reason why the financial advisor community eased its way into the world of AI instead of bounding in with both feet.

Now, however, it looks like the scale is tilting in favor of comfort and adoption on matters related to AI, as opposed to caution and inertia.

Case in point: Two years ago, Eric Ludwig, director of The American College Center for Retirement Income, would only get a smattering of hands when he asked groups of advisors if they were using AI in their practices. Fast-forward to today, and he sees 75 percent of hands go up.

“More financial planners are incorporating AI within their tools, whether FAs realize it or not, and I think that will be more the trend instead of standalone AI products,” Ludwig says. “In other words, AI could be part of an FAs financial planning software as opposed to a separate product.”

For those who haven’t started using AI yet, Ludwig maintains that there are a few reasons why, but most commonly it’s that they simply don’t know how to get started.

BECOMING COMFORTABLE WITH AI

“Our comfort level varies with the functionality where AI is being used,” says Mohan Gurupackiam, chief information officer at Steward Partners. “There are areas, including chatbots, note-taking, and AI assistants, where we are very comfortable.”

Those technologies, along with cybersecurity, generally have a low entry barrier to usage and are more easily adopted. Gurupackiam adds that he is quite comfortable with using AI for operational efficiencies, such as in data extraction from documents.

Areas that are still emerging and awaiting regulatory guidance are where wealth managers may prefer to wade in, rather than dive, according to Gurupackiam. Those include investment management and market research, where guidelines for establishing fiduciary responsibilities are still being developed.

Meanwhile, Dave Alison, president and founding partner of Prosperity Capital Advisors, has been using AI for the past three years and says he is very comfortable with its capabilities, so much so that he’s shifted his focus to improving his prompt-engineering with tools like ChatGPT.

“We are also using new AI tools in our business operations, such as Zocks for AI note-taking and creating automations for task and CRM management,” Alison says.

Likewise, Terry Parham Jr., co-founder and financial planner at Innovative Wealth Building, says he feels very comfortable with AI based on what he currently knows and uses it for. At the same time, however, he regularly asks AI about its most useful features, lesser-known capabilities, or ways that it could support his business more effectively.

“I believe comfort comes from both learning and doing, so I’ve made it a priority to build knowledge while also gaining hands-on experience,” Parham says.

GETTING INTELLIGENT ABOUT AI

Gurupackiam says there are multiple areas that he monitors to educate himself on the latest AI innovations. As Steward is a “cloud-native firm,” he constantly keeps an eye on emerging marketplace applications in the cloud to identify and use them within its technology stack. He also periodically evaluates emerging wealth technology platforms to identify their potential for use within Steward and integrate them as needed.

Another way of learning about AI is by attending technology conferences and support groups. Dave Valdez, partner and chief operating officer at Alaska Wealth Advisors, is a firm believer in the benefits of attending industry forums and joining CEO/COO/CTO groups that stay current with all the changes.

“I see it being a huge productivity driver for research, communication, and task management,” Valdez says. “We also see it being a valuable tool for advisor development and training. It’s going to help us analyze data more efficiently, both on our business and on our clients, so we can drive more value.”

Despite the increasing number of conferences nationwide dedicated to helping wealth managers improve their AI skills, Innovative Wealth Building’s Parham stays updated on the latest AI advancements without even leaving his desk. Instead, he watches YouTube tutorials, attends webinars, and explores content specific to financial professionals.

“The American College offers material focused on how AI can be applied in financial planning, which helps me stay informed without having to spend hours doing research on my own,” Parham says. “I also follow AI experts on LinkedIn and other platforms to keep up with how they’re using the tools and what trends they’re noticing.”

THE PRICE OF AI ADMISSION

An education on Wall Street costs money, as the old saying goes. And that doesn’t only apply to losing money on a stock or overpaying a fund manager. It also relates to spending on new technologies to keep pace with competitors.

The key with AI outlays, according to financial advisors, is to keep expenditure to a minimum as the technology evolves, without skimping so much that you’re left behind other IRAs. Parham, for example, says he is not spending a significant amount on AI at the moment as many of the tools available are free or very low cost.

“That will likely change over time as more AI tools begin charging for advanced features, especially those related to customization and automation,” Parham says.

He adds that a lot of the software that advisors already use has AI built in, so many people are using AI without even realizing it – or feeling like they’re explicitly paying for it.

Alison says he spends between $150,000 and $250,000 on AI across Prosperity’s offices. Furthermore, he expects that number to greatly increase as the firm adds to its productivity and efficiency resources.

Alaska Wealth’s Valdez, on the other hand, doesn’t currently have a line item specifically for AI spending. However, he acknowledges that his overall technology spend – including on AI – is rising.

“I see bespoke technology architecture as a necessary future spend for our firm as we continue to enhance client experience, improve our depth in knowledge, and seek efficiencies,” Valdez says.

THE ULTIMATE VISION FOR AI

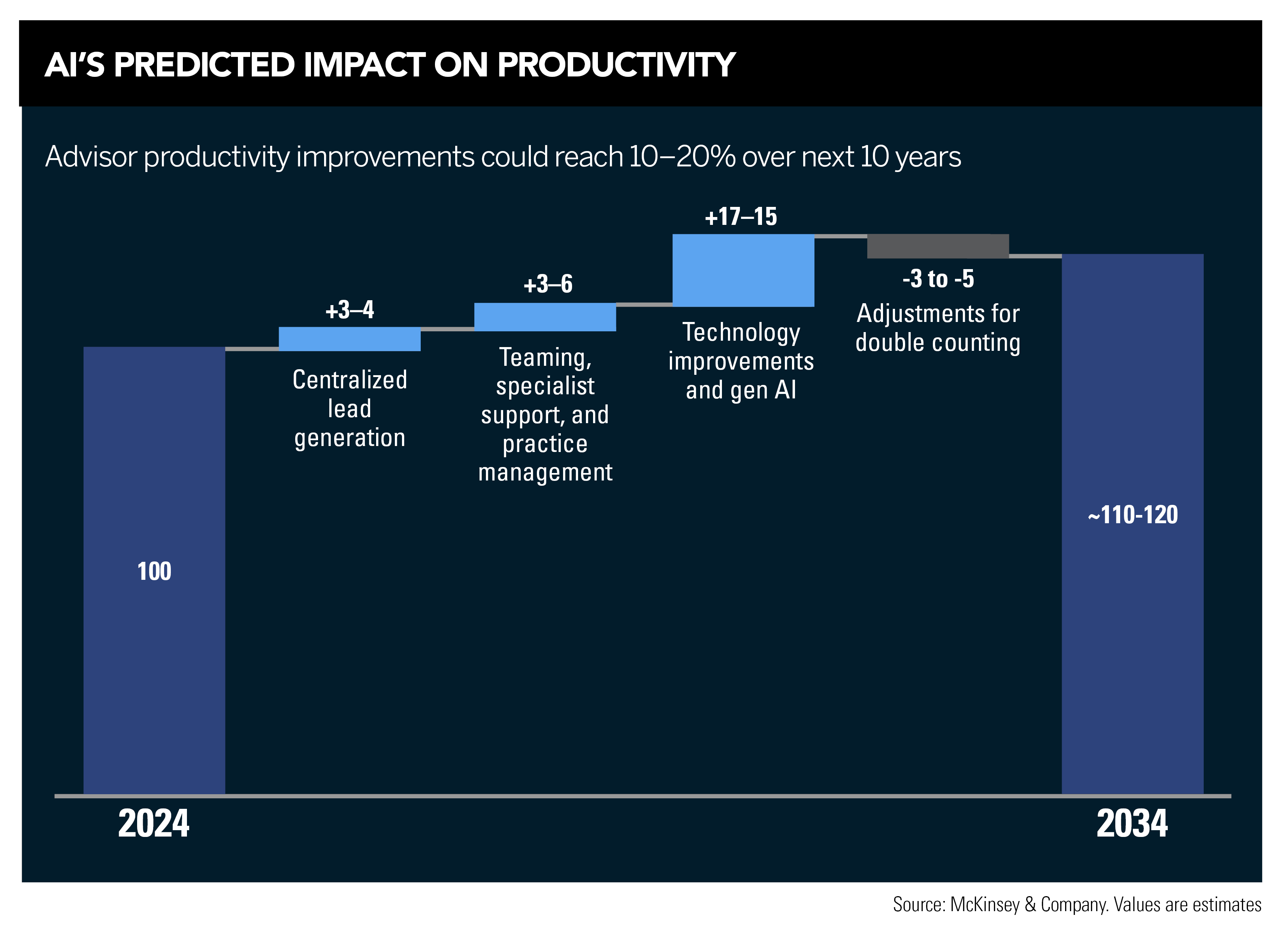

A recent McKinsey study estimates that the advisor shortage will reach around 100,000 in the next 10 years. Replacing all those advisors won’t be easy. Most likely, it will take AI to plug that big hole.

“Our industry is facing multiple challenges,” Gurupackiam says. “Increasing wealth and willingness to use human-centric advice, as well as a declining advisor head count, add pressure to increasing efficiency in wealth management firms.”

Not that AI will entirely replace the human touch of wealth managers. Heather Welsh, senior vice president at Sequoia Financial Group, says “AI will allow us to further tailor our solutions to individual client needs. It will not replace the role of our advisors but rather will enhance their interactions with our clients.”

Finally, financial advisors are not expecting the AI revolution to culminate in a big disruptive bang either. For all the talk of displacement and dislocation due to AI, the widespread belief among wealth managers is that it will ultimately be used as just another tool to better serve clients.

“I envision it running quietly in the background, pulling real-time information that previously required manual research,” Parham says. “It could enable advisors and clients to meet in virtual environments and interact with their own financial data in real time. Tasks that currently take multiple steps could become seamless and instant, helping us create a more personalized and efficient experience.”

{kind=link}