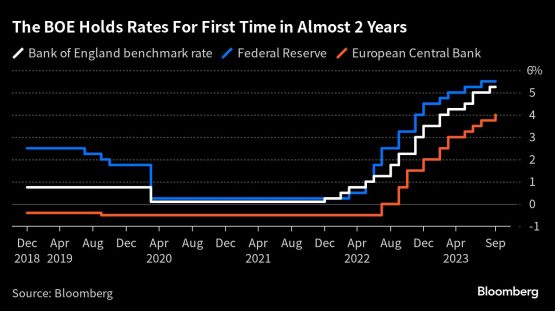

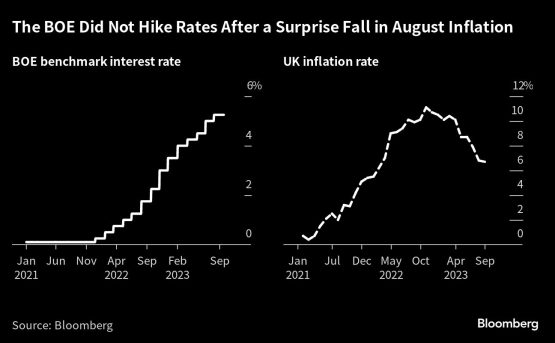

The Bank of England halted the most aggressive cycle of interest-rate rises in more than three decades amid falling inflation and mounting fears of recession.

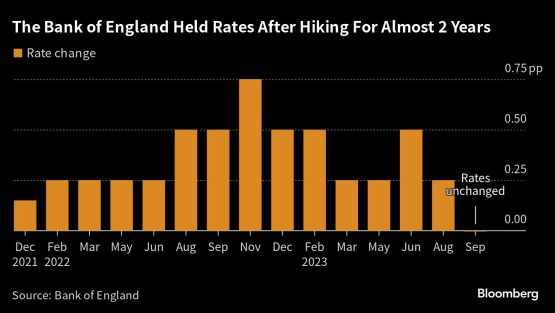

The central bank held its key rate at 5.25%, ending a series of 14 successive hikes since December 2021, when rates were just 0.1%. Five members of the Monetary Policy Committee voted to leave rates unchanged and four wanted to raise them to 5.5%. Governor Andrew Bailey, who had the casting vote, chose to hold.

ADVERTISEMENT

CONTINUE READING BELOW

The pound fell to the weakest since March against the dollar as traders trimmed bets on further interest-rate hikes. Markets were split before the decision, betting on a roughly 50% chance of a vote to hold, after data showed inflation unexpectedly fell in August.

Traders are now pricing in less than a full quarter-point increase of further tightening over the coming months. Goldman Sachs and Nomura said on Wednesday that rates have probably already peaked. Sterling traded as much as 0.9% weaker at $1.2239, taking a slide over the past month to around 4%, the biggest decline across Group-of-10 peers.

What Bloomberg Economics Says …

“The Bank of England is probably done with lifting interest rates. While its guidance continues to suggest more hikes could yet come if signs of greater inflation persistence emerge, the data has turned in a dovish direction and is unlikely to cause enough alarm for the central bank to hike again. We now expect interest rates to remain on hold until the second half of 2024.”

—Dan Hanson and Ana Andrade, Bloomberg Economics.

The decision will come as a relief to millions of households facing the threat of even higher mortgage costs and indebted businesses. It will also be welcomed by Prime Minister Rishi Sunak, who has promised to ease the inflation crisis and improve living standards ahead of an election expected next year.

The BOE, however, signaled that policy was only on pause and it would respond if inflation, which remains more than three times above the 2% target, doesn’t fall as expected. The MPC forecasts consumer-price inflation to hit the target in the second quarter of 2025.

“Inflation has fallen a lot in recent months and we think it will continue to do so,” Bailey said in a written statement. “That’s welcome news. But there is no room for complacency. We need to be sure inflation returns to normal and we will continue to take the decisions necessary to do just that.”

Chancellor of the Exchequer Jeremy Hunt told Bailey in a letter than the MPC has his full support. “The tough action taken by the MPC to squeeze inflation out of the system is working,” Hunt said, adding that the government needed to show fiscal discipline to bolster the bank’s actions.

Repeating its former guidance, the committee said rates would be “sufficiently restrictive for sufficiently long” and “further tightening in monetary policy would be required if there were evidence of more persistent pressures.” Like other major central banks, the implication is that rates would remain high for longer.

“We are starting to see the tide turn against high inflation, but we will continue to do what we can to help households struggling with mortgage payments,” Hunt said in a statement from the Treasury. “Now is the time to see the job through. We are on track to halve inflation this year and sticking to our plan is the only way to bring interest and mortgage rates down.”

A halt to the quickest series of rate hikes in three decades is a relief for businesses and consumers, who have seen borrowing costs rocket since the end of 2021, bringing to an abrupt halt an era where the cost of loans was near historic lows.

“Many small firms have suffered financially, with margins and cash reserves battered by both the phenomenon the Bank tried to control, inflation, and the ‘cure’ it applied, leading to higher borrowing costs and dampened consumer demand,” said Martin McTague, chair of the Federation of Small Businesses.

The MPC has been laying the ground to pause policy as the UK’s economic outlook darkened in recent weeks. Bailey said this month that rates were “much nearer now to the top of the cycle” and Deputy Governor Jon Cunliffe said the bank was close to a turning point.

The MPC expressed concerns that the economy was stalling after output in July contracted 0.5%, a sharper fall than expected, and official figures showed unemployment rising and job vacancies dropping. The committee also noted that business activity data is contracting, while raising questions about official measures that show wage growth is accelerating.

The BOE cut its GDP growth forecast for the third quarter to 0.1% from 0.4%, the minutes showed. Underlying growth in the second half of 2023 is also likely to be weaker than the 0.25% expected in August.

The bank said past rate hikes were having an impact: “There are increasing signs of some impact of tighter monetary policy on the labor market and on momentum in the real economy more general.”

As the economy slows, inflation was expected to drop below 2% “in the medium term.” In the short term, the bank expects a “significant” fall in inflation “despite the renewed upward pressure from oil prices” due to declining energy and goods inflation.

Higher rates have been punishing homeowners, who face a £15 billion repayment crunch, according to the Resolution Foundation, much of which has yet to come through. Several MPC members have been warning that policy lags mean the BOE was already at risk of overtightening.

Swati Dhingra, an external member has been voting to hold since December last year. She was joined by Bailey, Deputy Governors Ben Broadbent and Dave Ramsden and Chief Economist Huw Pill. Cunliffe and external members Megan Greene, Catherine Mann and Jonathan Haskel voted to raise rates by a quarter point to 5.5%.

Other central banks are signalling that cycle is over, too. The ECB raised rates to 4% last week and said “sufficient contributions” had been made to return inflation to target. The US Federal Reserve on Wednesday held rates in the 5.25%-5.5% range, but did suggest further increases were on the cards and ruled out any imminent rate cuts.

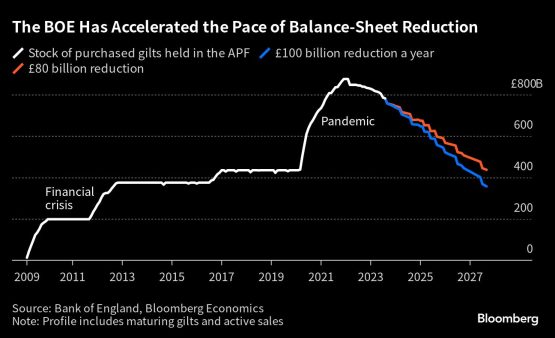

The BOE also stepped up the pace of quantitative tightening as it seeks to reduce the size of its balance sheet as quickly as possible to provide headroom for potential future financial stability interventions.

Over the 12 months from October, it plans to reduce its gilt portfolio by £100 billion to £658 billion. Last year, it unwound £80 billion. That implies £50 billion of active gilt sales on top of the £50 billion of maturing assets. The gilt portfolio peaked in 2022 at £875 billion.

© 2023 Bloomberg

{kind=link}