By John Kourkoutas

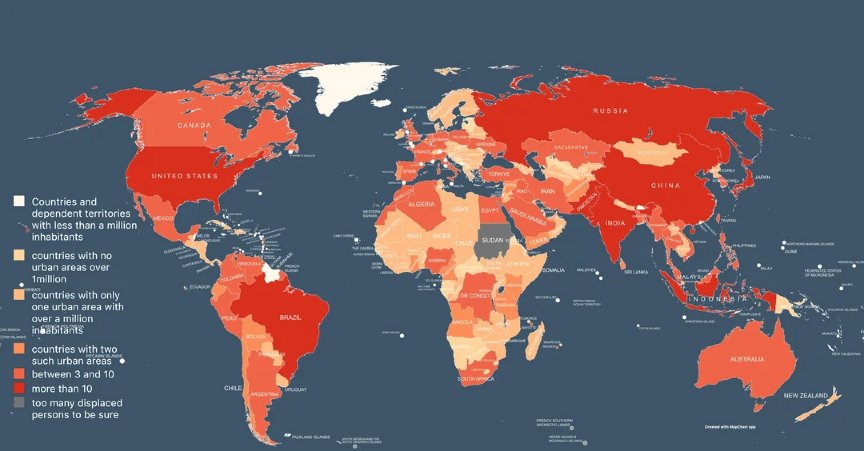

Look at a map of urban agglomerations below – cities with populations exceeding one million – and a stark pattern emerges. The United States, China, India, Brazil, and Russia are drenched in deep red: ten or more megacities each, sprawling networks of economic gravity.

Most of Africa, by contrast, registers a pale orange or yellow. Zero cities. Or one.

That solitary dot is not a data anomaly. It is a structural reality with profound consequences for any business operating on the continent. Economists call it the “primate city” problem, and understanding it is arguably the single most important piece of urban intelligence for companies considering African market entry.

One City to Rule Them All

In the majority of African nations, a single urban center dominates the national economy with a concentration of power that has no equivalent in the developed world. Government ministries, financial institutions, logistics networks, distribution infrastructure, and the bulk of skilled talent all converge in one place.

Consider Zambia. Lusaka is not merely the capital – it is the economy. Every meaningful transaction, regulatory interaction, and supply chain node flows through it.

Tanzania presents a slight variation: while Dodoma holds the formal designation of capital, Dar es Salaam drives commercial life with a grip that administrative rebranding has done little to loosen.

Kenya stands as one of the continent’s more mature urban exceptions, with both Nairobi and Mombasa functioning as genuine economic poles. Nigeria is the outlier that proves the rule: Lagos, Abuja, Kano, and Port Harcourt constitute a rare multi-nodal urban system on a continent where such configurations are the exception, not the norm.

For the vast majority of African countries, however, one city carries the entire weight of a nation’s urban economy.

The Double-Edged Sword of Concentration

For a European company scoping African expansion, the primate city dynamic cuts both ways – and executives who fail to reckon with both edges tend to end up on the wrong side of one of them.

The opportunity is deceptively elegant. Market entry, in structural terms, is simpler than it appears.

There is no need for a fifteen-city rollout strategy, no requirement to simultaneously cultivate regional hubs across a vast geography. Win the primate city first, and you have, in most cases, won the market. The concentration of consumers, institutions, and intermediaries that would take years to assemble in a polycentric market already exists – waiting, in a single urban address.

The risk is the mirror image of that same fact. If your Lusaka strategy fails, there is no fallback. No secondary market to absorb the pivot, no adjacent city with comparable infrastructure or purchasing power where the playbook can be quietly retested. In a multi-city market, failure is recoverable. In a primate city market, it can be terminal for a regional strategy.

The Wave That Is Coming

This calculus, however, is shifting – and the pace of that shift is where the real strategic story lies.

Africa is urbanizing faster than any region in recorded history. The United Nations projects that the continent’s urban population will more than double by 2050, adding hundreds of millions of city dwellers in a compressed timeframe that Europe and North America took well over a century to traverse.

That growth is not flowing exclusively into existing megacities. It is filling secondary and tertiary urban centers that currently register below the threshold of global business attention.

In Zambia, Ndola, Kitwe, and Livingstone are expanding. In Tanzania, Mwanza and Arusha are developing genuine economic identities independent of Dar es Salaam.

In Kenya, Eldoret and Nakuru are absorbing population and commercial activity at rates that will soon demand a reappraisal of the standard two-city model. Ghana’s Kumasi is already straining the limits of what “secondary city” can mean.

The companies that establish themselves in these markets now – before the population crosses the one-million threshold, before the infrastructure investment follows, before the competitive set arrives – will occupy a position of structural advantage that late entrants will find extraordinarily difficult to dislodge.

Where the Smart Money Is Looking

The scramble for Lagos, Nairobi, and Johannesburg is well underway. The competition is fierce, the valuations reflect the attention, and the first-mover advantages have long since been claimed.

That race has largely been run.

The next race – for the cities not yet visible on the global map of mega-urban concentration – has barely begun. The primate city problem, for those willing to think one urbanization cycle ahead, is not a constraint. It is a map. And the most valuable territory on it is still, for the moment, unclaimed.

John Kourkoutas is business development expert that specializes in helping companies, export teams, and business leaders succeed in Africa’s dynamic and emerging markets.

{kind=link}