These notices, sent by SARS Debt Management, appear to focus on more recent trust debt for now. However, once received, time is of the essence.

SARS has consistently emphasised the need for trusts to comply by ensuring that all tax returns and outstanding liabilities — both current and historical — are up to date. After years of perceived leniency towards trusts, this shift toward filing civil judgments to recover tax debt marks a significant development that trusts and trustees should take seriously.

André Daniels, Head of Tax Controversy & Dispute Resolution at Tax Consulting South Africa, stresses that these notices are more serious than they may initially appear.

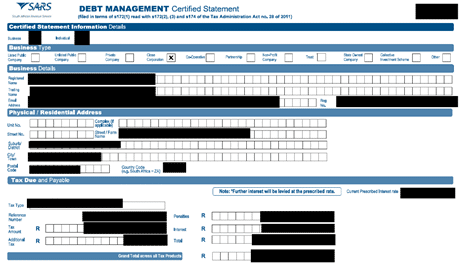

“When you reach this stage, SARS only needs to provide the court with a 2- or 3-page debt management certified statement of taxes due and payable, including interest and penalties. The registrar or clerk of the court can rubber-stamp the statement, giving it the effect of a civil judgment issued by the relevant court.”

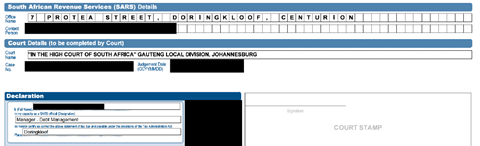

This is an example of what SARS takes to court:

This notification may follow:

Legal Basis for SARS’ Civil Judgment Powers

While it may seem harsh, this is in line with the powers awarded to SARS in the Tax Administration Act (TAA), Part B of Chapter 11 dealing with the judgment process, stating:

“If a person has an outstanding tax debt, SARS may, after giving the person at least 10 days’ notice, file with the clerk or registrar of a competent court a certified statement setting out the amount of tax payable and certified by SARS as correct.”

It further reads: “SARS is not required to give the taxpayer prior notice under subsection (1) if SARS is satisfied that giving notice would prejudice the collection of the tax.”

“A certified statement filed under section 172 must be treated as a civil judgment lawfully given in the relevant court in favour of SARS for a liquid debt for the amount specified in the statement.”

Daniels reiterates that it is important to adhere to SARS correspondence regarding outstanding debt and make full use of grace periods the tax authority provides, as well as measures to address the tax liability.

Receiving a final letter of demand means leniency is coming to an end. Taxpayers should act immediately to avoid SARS collection steps. In a final letter of demand, SARS affords the taxpayer the opportunity to apply for one of the following:

- Payment in instalments if unable to pay the full amount once-off

- Suspension of debt where the taxpayer has or intends to submit a formal dispute

- Compromise of a portion of the tax where this will mean a higher return to the fiscus than liquidation, sequestration, or other collection measures

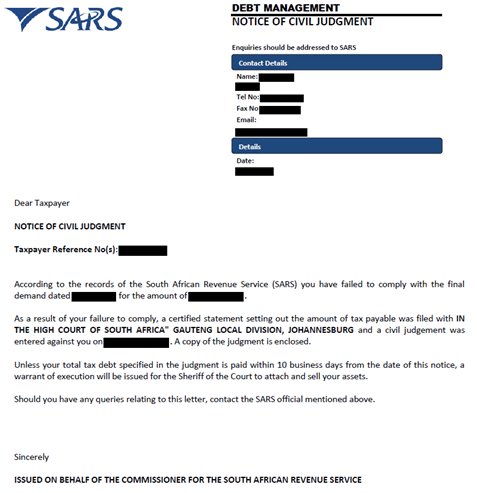

As such SARS also clearly warns that failure to comply with the final demand, may result in SARS appointing 3rd parties to withhold money on their behalf, or that it may lead to civil judgment, in which case a warrant of execution may be issued for the Sheriff to attach and sell assets of the indebted taxpayer.

According to Daniels, there are many cases where SARS even follow-up with a “courtesy request” as a reminder for outstanding debt, showing SARS’ leniency and encouraging trusts to comply and regularise their tax affairs, before opting for civil judgment.

An Important Step in SARS’ Enhanced Focus on Trusts

After years of addressing the issue of historic non-compliance among trusts, SARS on 9 February 2026, communicated that it has issued final demands to trusts who did not submit an annual tax return for the 2024 and 2025 years of assessment. It warned recipients to take steps to correct non-compliance and avoid penalties.

The tax authority appears to be focusing on recent trust tax debt rather than historical liabilities, presumably viewing it as low hanging fruit and more readily recoverable than amounts outstanding for many years.

Tax debt is on SARS’s radar and the message is clear: if SARS allows trusts the opportunity to settle outstanding amounts, address the tax liability through the dispute resolution process, or make alternative payment arrangements, it is a chance to get it right.

{kind=link}