The Central Bank of West African States (BCEAO) has quietly rewritten a key rule of engagement for the region’s financial system.

Under a new regulatory notice published this week, the millions-strong West African diaspora can now open and hold local CFA franc bank accounts from abroad under the exact same conditions as residents.

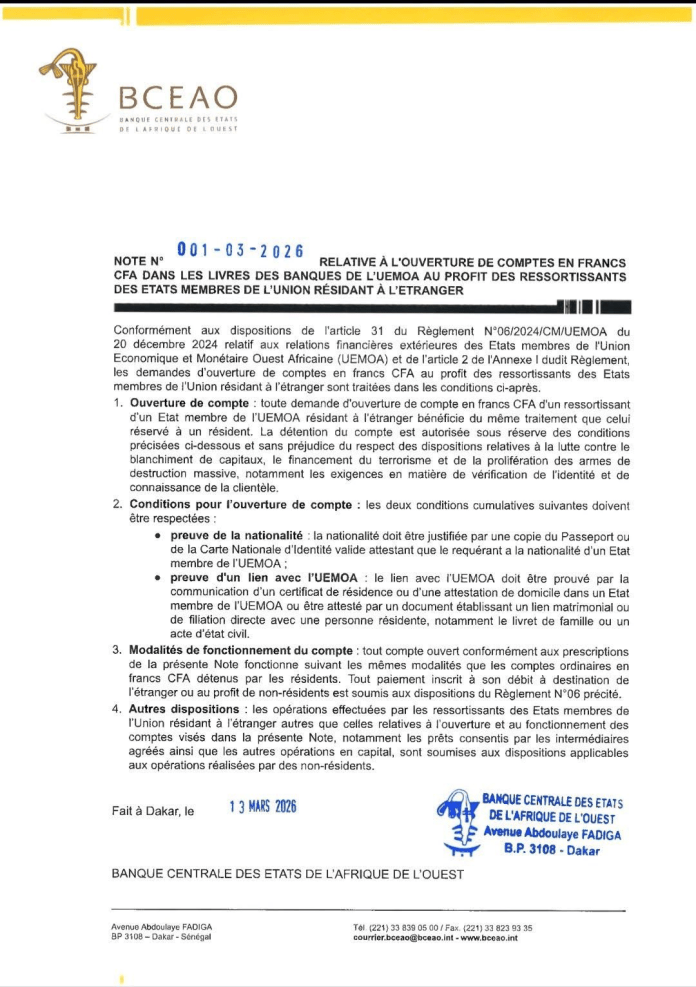

The policy shift, outlined in Notice №001–03–2026 signed on March 13, effectively turns external remitters into local banking clients. For the financial technology companies and commercial banks operating across the West African Economic and Monetary Union (WAEMU) — which includes Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal, and Togo — it opens up a massive, previously ring-fenced liquidity pool.

Historically, the diaspora has been treated as external to the formal domestic financial system. They could send money home via money transfer operators (MTOs) or fintechs, but could not easily hold, save, or manage funds as residents do. That distinction has now been erased.

The prize: A fragmented $10bn+ flow

Behind the policy sits a sizeable pool of capital. Across WAEMU’s eight member states, diaspora inflows are estimated in the low double-digit billions annually.

Senegal alone received 2,211 billion CFA francs (approximately $3.8bn) in remittances in 2024, representing nearly 12% of the country’s GDP. These flows have become a source of foreign currency larger than public development aid, leading Senegalese Prime Minister Ousmane Sonko to recently describe the diaspora as the country’s “financial gold.”

However, these flows have traditionally been operationally off-balance sheet for local banks, dominated by cash-out models rather than deposit mobilisation. The BCEAO’s move defocuses increasing the volume of inflows; rather it aims to bring changes to where that money sits once it arrives.

For startups and digital players, the implications are structural. The reform creates new revenue lines across the financial stack, forcing a pivot from pure remittance models to comprehensive wealth management and neobanking.

- Neobanks and Digital Wallets: Startups operating in cross-border payments can now position themselves around remote KYC and app-based diaspora banking interfaces. It is a major product expansion moment; instead of taking a 1% cut on a transfer, fintechs can now capture the underlying deposit and offer savings, bill payments, and credit products.

- Commercial Banks: Traditional banks gain a direct route to diaspora deposits in CFA, offering a low-cost liquidity opportunity for a sector long constrained by shallow deposit bases.

- Traditional MTOs: The shift introduces a structural risk for legacy remittance players. With funds now able to land directly into resident bank accounts, reliance on vast, expensive cash pick-up networks will likely decrease.

The end of the closed loop

The diaspora banking reform does not exist in a vacuum. It follows the BCEAO’s systematic dismantling of the silos that previously characterised the region’s digital financial landscape.

In September 2025, the central bank launched the Interoperable Instant Payment System Platform (PI-SPI), mandating instant transfers between banks, mobile money operators, and fintechs. Users can now send money across platforms — such as from Wave to Orange Money or MTN MoMo — without additional transfer fees.

The combination of full interoperability and diaspora account access creates a highly competitive environment. For established players like Wave, whose closed-loop model transformed the market, the new landscape reduces the competitive advantage of forced customer loyalty. Competition will now be dictated by service quality, user experience, and the ability to monetise new use cases beyond basic transfers.

The regulatory fine print

Despite the commercial opportunities, the reform is an incremental recalibration rather than a total liberalisation of capital flows.

To open an account under the new rules, applicants must meet two cumulative conditions:

- Proof of nationality: A valid passport or national ID from a WAEMU member state.

- Proof of regional ties: A residence certificate, proof of domicile in a member state, or a civil status document demonstrating direct family ties with a resident.

Crucially, while the policy widens the current account to encourage inflows, capital controls on outflows remain intact. Transfers abroad or for the benefit of non-residents remain subject to existing foreign exchange rules under Regulation №06/2024/CM/UEMOA. Anti-money laundering (AML) and counter-terrorism financing provisions, including stringent KYC requirements, also remain fully in force.

What comes next

The BCEAO’s strategic intent is clear: internalise informal flows into the banking system, deepen domestic deposit bases, and pull the formal banking sector back into relevance for diaspora finance amid the rise of crypto and digital wallets.

Execution will determine how much of the multi-billion-dollar flow actually migrates onshore. Digital onboarding friction, trust gaps with domestic banks, and pricing differentials will be the immediate hurdles to clear.

But the regulatory pathway has been built. For West African fintechs, the race is now on to build the products that will convince the diaspora to park their money at home.

{kind=link}